This givesyou the balance to compare to the income statement, and allows youto double check that all income statement accounts are closed andhave correct amounts. If you put the revenues and expenses directlyinto retained earnings, you will not see that check figure. Nomatter which way you choose to close, the same final balance is inretained earnings.

Post navigation

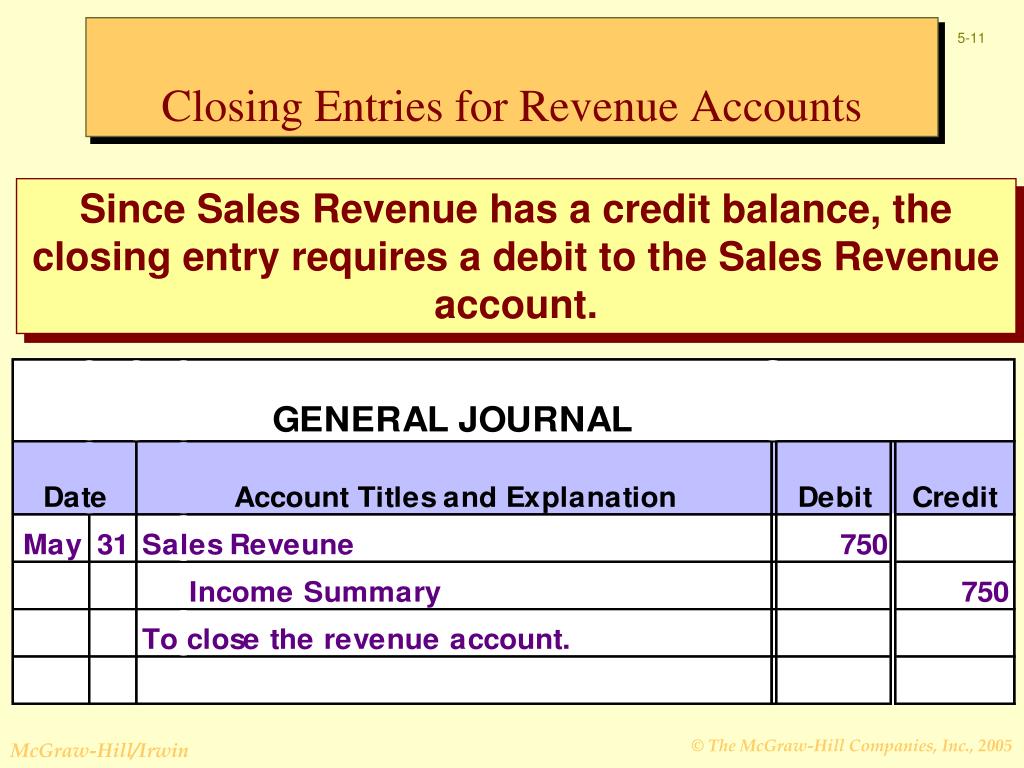

Remember that all revenue, sales, income, and gain accounts are closed in this entry. Any account listed on the balance sheet is a permanent account, barring paid dividends. On the balance sheet, $75 of cash held today is still valued at $75 next year, even if it is not spent. Let’s move on to learn about how to record closing those temporary accounts. Income and expenses are closed to a temporary clearing account, usually Income Summary. Afterwards, withdrawal or dividend accounts are also closed to the capital account.

Example of Closing Entry

- This trial balance gives the opening balances for the next accounting period, and contains only balance sheet accounts including the new balance on the retained earnings account as shown below.

- They offer an overview of a business’s financial position at the end of the applicable accounting period, whether that’s the previous month or year.

- They arealso transparent with their internal trial balances in several keygovernment offices.

- We’ll use a company called MacroAuto that creates and installs specialized exhaust systems for race cars.

Debit each revenue account and credit the Income Summary account. An accounting year-end which is not the calendar year end is sometimes referred to as a fiscal year end. Kristin is a Certified Public Accountant with 15 years of experience working with small business owners in all aspects of business building.

The Purpose of Closing Entries

Now, all the temporary accounts have their respective figures allocated, showcasing the revenue the bakery has generated, the expenses it has incurred, and the dividends declared throughout the past year. The retained earnings account is reduced by the amount paid out in dividends through a debit and the dividends expense is credited. The next and final step in the accounting cycle is to prepare one last post-closing trial balance.

The balance sheet’s assets, liabilities, and owner’s equity accounts, however, are not closed. These permanent accounts and their ending balances act as the beginning balances for the next accounting period. Now that the revenue account is closed, next we close the expense accounts.

Step 1: Close all income accounts to Income Summary

A closing entry is a journal entry that’s made at the end of the accounting period that a business elects to use. It’s not necessarily a process meant for the faint of heart because it involves identifying and moving numerous data from temporary to permanent accounts on the income statement. Temporary (nominal) accounts are accounts thatare closed at the end of each accounting period, and include incomestatement, dividends, and income summary accounts. If the total debits and credits in your trial balance are the same, you’re ready to produce a balance sheet and income statement (also known as a “profit and loss report” or “P&L”). These reports can be generated automatically in your accounting software.

The four-step method described above works well because it provides a clear audit trail. For smaller businesses, it might make sense to bypass the income summary account and instead close temporary entries directly to the retained earnings account. The closing entries are also recorded so that the company’s retained earnings account shows any actual increase in revenues from the prior year and also shows any decreases from dividend payments and expenses. As the drawings account is a contra equity account and not an expense account, it is closed to the capital account and not the income summary or retained earnings account.

In this guide, we delve into what closing entries are, including examples, the process of journalizing and posting them, and their significance in financial management. In this example we will close Paul’s Guitar Shop, Inc.’s temporary accounts using the income summary account method from his financial statements in the previous example. In some cases, accounting software might automatically handle the transfer of balances to an income summary account, once the user closes the accounting period. The entries take place “behind the scenes,” often with no income summary account showing in the chart of accounts or other transaction records. Suppose a business had the following trial balance before any closing journal entries at the end of an accounting period.

At the core of this suite is the Financial Close Management solution, which simplifies and accelerates financial close activities, ensuring compliance and reducing errors. We’ll use a company called MacroAuto that creates and installs specialized exhaust systems for race cars. Here are MacroAuto’s accounting records simplified, using positive numbers for increases and negative numbers classified balance sheet for decreases instead of debits and credits in order to save room and to get a higher-level view. To close the drawing account to the capital account, we credit the drawing account and debit the capital account. Notice that the balance of the Income Summary account is actually the net income for the period. Remember that net income is equal to all income minus all expenses.

Balances from temporary accounts are shifted to the income summary account first to leave an audit trail for accountants to follow. Income summary is a holding account used to aggregate all income accounts except for dividend expenses. It’s not reported on any financial statements because it’s only used during the closing process and the account balance is zero at the end of the closing process. Temporary account balances can be shifted directly to the retained earnings account or an intermediate account known as the income summary account. The net income (NI) is moved into retained earnings on the balance sheet as part of the closing entry process. The assumption is that all income from the company in one year is held for future use.